Scalable Capital’s €155 million funding round underscores a broader trend: European wealthtechs evolving from technology to fully regulated digital institutions.

The European wealthtech landscape is undergoing a fundamental transformation. No longer confined to algorithmic automation or digital onboarding, leading platforms are evolving into institutional-grade financial ecosystems. This shift is exemplified by Scalable Capital‘s recent €155 million funding round, led by Sofina and Noteus Partners, bringing its total funding to over €470 million.

Scalable Capital’s ambition to become the “Charles Schwab of Europe” reflects a broader movement among fintechs to transition from niche digital services to comprehensive, regulated financial institutions. The company plans to expand into France and Italy and aims to grow client assets from €30 billion to over €100 billion within the next two to three years.

End of the Robo-Advisor/Neo-Broker Innocence

The robo-advisory/neo-broker era introduced efficiency and accessibility to personal investing. However, we are now entering a post-algorithmic phase, where the ambition is not just to digitalize services but to redefine the operating model of wealth intermediation itself. Platforms like Scalable Capital, Trade Republic, Moneyfarm and Bitpanda are building vertically integrated ecosystems encompassing investment management, brokerage, pensions, tax services, and increasingly, full banking capabilities.

This strategy is echoed across Europe:

- Trade Republic (Germany) combines brokerage with savings products and holds a German banking license, positioning itself as a full-service investment hub.

- Moneyfarm (Italy/UK) blends human advice with digital infrastructure and is progressively enriching its product suite across Europe.

- Bitpanda (Austria) started in crypto, but now offers stocks, ETFs, and savings, having secured an investment firm license.

These examples show a common trajectory: from feature to ecosystem, from interface to infrastructure.

Banking Licenses: Infrastructure for Digital Trust

The pursuit of banking licenses by fintech platforms is not merely about expanding services or margins; it’s about legitimacy. In a fragmented European regulatory environment, trust cannot be improvised it must be engineered. A banking license serves as a systemic foundation, signaling institutional maturity and enabling operations across borders with credibility and control.

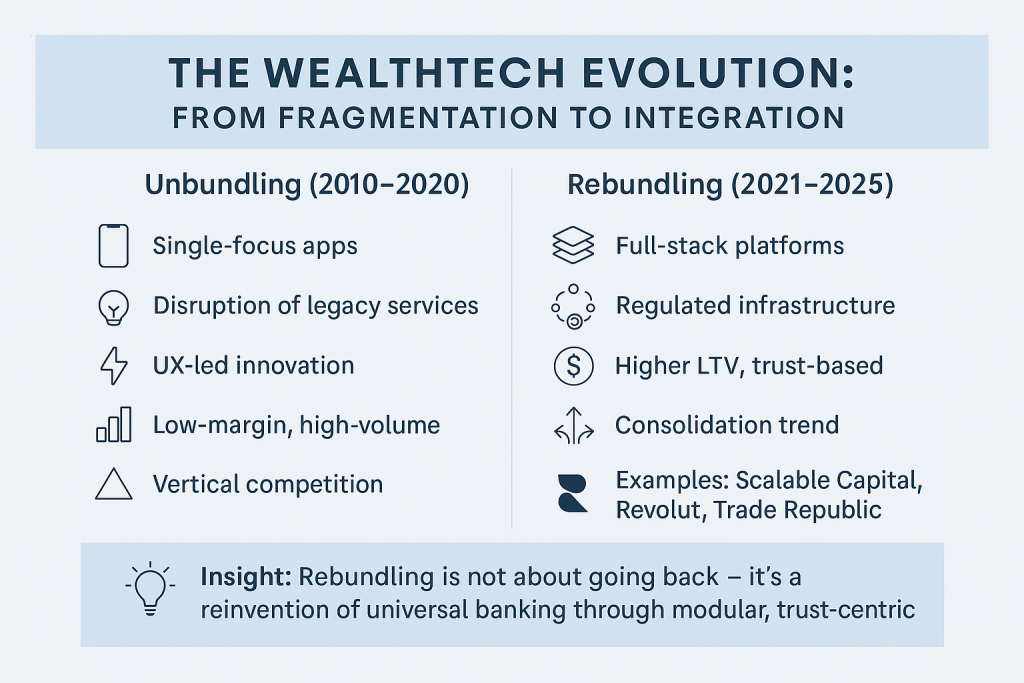

From Unbundling to Rebundling

The European fintech ecosystem is now entering what could be called its “rebundling phase.” For over a decade, the sector experienced an unbundling of traditional banking functions: startups focused on narrow, high-impact services, currency exchange, peer-to-peer payments, robo-advisory or low-cost trading.

This fragmentation was a necessary stage: it demonstrated that legacy banks could be challenged on user experience, efficiency and accessibility.

Now, we are witnessing a strategic shift: leading platforms are rebundling services into coherent, full-stack digital ecosystems.

This rebundling is not a return to the past. It is a reconstruction of universal banking on digital-native infrastructure, with a renewed focus on trust, transparency and cross-service integration.

Ecosystems Over Interfaces

The emerging trend is not just about better apps but about creating financial habitats where wealth management becomes an ongoing experience rather than a discrete transaction. These platforms are moving toward “total wealth access”, offering multi-asset, multi-goal investing, banking and payments integration, cross-border consistency, and embedded education and behavioral nudges.

Strategic Convergence: When Fintech Meets the Institutional Core

The influx of capital from incumbents such as BlackRock, Allianz and J.P. Morgan signifies a strategic alignment: retail intermediation is the next frontier of platform economics. However, this convergence brings tension will fintech remain independent or become a vessel for traditional distribution in digital attire? Governance, transparency, and API-based modularity will determine whether these ecosystems remain open or become captive architectures.

The Human Factor: Relational Sustainability in a Digital World

Technology alone cannot solve the fiduciary paradox. Wealth management is not just about data and optimization: it’s about time, trust and human intention. As digital platforms mature, preserving the relational dimension of finance becomes paramount. The challenge lies in embedding relational continuity within scalable digital infrastructures.

Conclusion: From Product to Purpose, From Interface to Infrastructure

European wealthtech is maturing. The new wave is not about apps or pricing wars, it’s about infrastructural trust at scale. The question is no longer: “Can we digitalize wealth management?” We already have. The real question is: “Can we build digital ecosystems that sustain trust over time?“

Only those who answer this will earn the right to become the next financial institutions of Europe.

Lascia un commento